The tax-exempt benefit to heirs of a Roth is especially important for those subject to the estate tax, because heirs who would have to pay the estate tax would also have to pay an income tax if they inherited a traditional IRA.

Many clients hold substantial assets in tax-deferred retirement accounts, such as traditional IRA’s and workplace retirement plans. Depending on their goals, clients may want to think about converting some of or all those assets to a Roth IRA. Discussions around conversions most commonly focus on retirement planning and expectations for current and future tax rates. However, clients may not understand that Roth’s can also serve as a vehicle in an estate plan to help them achieve—or amplify—their wealth-transfer goals.

When clients convert from a traditional to a Roth IRA, they prepay the income taxes for beneficiaries. Additionally, if an estate is large enough to be subject to the federal estate tax, the conversion means heirs will not also have to pay income taxes on distributions, nor will they have to worry about tracking any cost basis, as they might with an inherited traditional IRA.

Both the growth within, and the qualified distributions from, a Roth account, are not subject to income tax, making a Roth a valuable structure for estate planning.

Potential to transfer greater after-tax wealth

From a wealth-transfer perspective, Roth IRAs have two advantages over traditional IRAs.

First, they do not require account owners to take required minimum distributions (RMDs) during their lifetime. The amounts that would be paid out in RMDs and subject to income tax in a traditional IRA can continue to grow in a Roth IRA tax-exempt. This could result in a greater account balance when the Roth IRA is ultimately transferred to beneficiaries.

Second, qualified Roth distributions are tax-exempt: No income tax is due when withdrawals are taken.

These features can substantially increase after-tax wealth for beneficiaries.

How clients pay the taxes due at conversion can also have a significant impact. Roth conversions may be either tax-exclusive or tax-inclusive. If clients pay the taxes due with assets outside the IRA, the conversion is tax-exclusive. This is often the better strategy because it transfers the entire pre-tax IRA balance to the Roth account, essentially increasing its after-tax value. On the other hand, in a tax-inclusive conversion, the income tax is paid from the traditional IRA and the beginning value of the Roth is reduced accordingly.2

Hypothetical scenarios

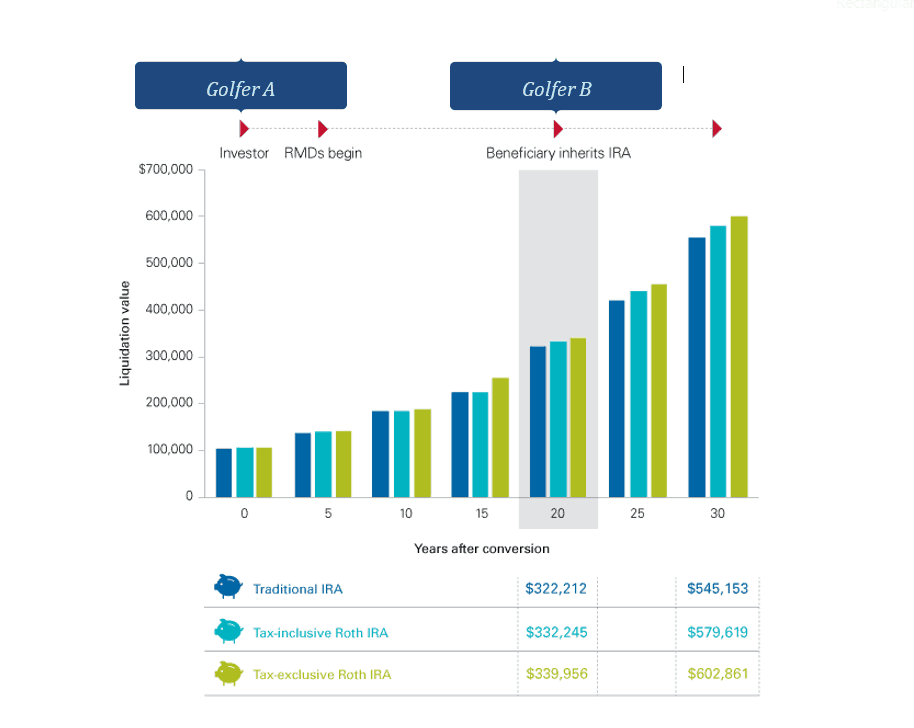

Consider a hypothetical 65-year-old client (Golfer A) with a taxable account balance of $24,000, a traditional IRA balance of $100,000, and a 40-year-old non-spouse beneficiary. In the following three scenarios, the account owner and beneficiary are in a 24% tax bracket, and Golfer B inherits the IRA and the taxable account 20 years after each scenario begins. The figure below shows the combined after-tax liquidation value of the IRA and the taxable account over time for the scenarios. For simplicity, we assume that no estate taxes are due at Golfer A’s death and that the income tax rate for both parties remains constant.

Scenario 1—No Roth used: Golfer A reinvests all income and dividends in both accounts. She begins taking RMDs from the traditional IRA at age 70½ and reinvests the after-tax proceeds in her taxable account. Upon inheriting the IRA, her beneficiary (Golfer B) begins taking RMDs according to his life expectancy—as is legally required—and reinvests them, net of taxes, into the taxable account.

Scenario 2—Use a Roth, and pay taxes from the Roth: Golfer A converts the entire traditional IRA to a Roth IRA at age 65 and pays the conversion taxes from the IRA (regular income that’s taxable) while maintaining the taxable account, leaving her with a $76,000 Roth IRA and a $24,000 taxable account. This would be the tax-inclusive Roth conversion. She does not take any withdrawals from the Roth during her lifetime. Upon inheriting the Roth, her beneficiary (Golfer B) takes RMD’s (exempt from income tax) based on his life expectancy and invests them in the taxable account.

Scenario 3—Use a Roth, but pay taxes from a source other than the Roth: Identical to Scenario 2, except the account owner pays the conversion taxes using the money in her taxable account, leaving her with $100,000 in her Roth IRA and no balance in her taxable account. This would be the tax-exclusive Roth conversion with the full balance converted.

As the figure below shows, converting to a Roth can lead to greater after-tax wealth being passed on to Golfer A’s beneficiary. This is especially true if the taxes on the conversion are paid with funds outside the IRA. Converting to a Roth initially reduces total wealth by the amount of the income taxes paid. However, because RMDs are not required during Golfer A’s lifetime, the balance of the Roth may be drawn down more slowly than what would happen with a traditional IRA. This means more of the Roth can benefit from tax-exempt compounding for longer, possibly resulting in significantly more wealth over time.

We preach this strategy as often as we can and although many of our clients don’t completely understand the enormous benefits at first, they realize the net worth building effect as they become older in retirement and are always thankful we had the foresight. If you’d like to know more about your situation and if there are strategies that might benefit your family, please contact us.

Notes:

- Amounts shown are the after-tax liquidation value of the accounts at the end of each year. Assumes a 6% annual rate of return on a 50% equity/50% fixed income portfolio, with all income and dividends reinvested. Distributions from the traditional IRA are taxed at a rate of 24%, dividends and long term capital gains in the taxable portfolio are taxed at a rate of 15%. Assumes the portfolio is rebalanced annually.

- Withdrawals from a Roth IRA are tax free if you are over age 59½ and have held the account for at least five years; withdrawals taken prior to age 59½ or five years may be subject to ordinary income tax or a 10% federal penalty tax, or both. (A separate five-year period applies for each conversion and begins on the first day of the year in which the conversion contribution is made.

- All investing is subject to risk, including the possible loss of the money you invest. We recommend that you consult a tax or financial advisor about your individual situation.

Blake Parrish, CFP®

Senior VP, Portfolio Manager

Phone: (503) 619-7237

E-mail: blake@bpfinancialassoc.com

Certified Financial Planner Boardof Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.”