Imagine you’re a PGA golf professional, but were also assigned the position of money manager, how would you do? Let’s say the job title is actually money manager for You Incorporated and you need to manage money for yourself better than at the facility you work for. Would you fire you, or keep the job? Wait, don’t actually answer that.

You have to tell your money what to do or it will leave you and go somewhere else. A written budget for the month is your money goal.

People who win at anything have written goals. Goals are what “YOU” are aiming at. There’s a famous saying that goes something like, “when you aim at nothing you’ll hit it everytime.” Accountability, commitment, and writing down one’s goals enhances goal achievement. Here’s a study to back it up.

Did you read The Millionaire Next Door when I mentioned it in a previous newsletter? The key to this story is to give every dollar a name before the month starts. Spend less than what you have coming in. How would you know these figures? Write it down. Give each dollar from your paycheck a name like, groceries, utility bills, insurance, rent/mortgage, gas, savings, dog food, tournament expense, etc. You must end the month where your income matches the expenses that were written down or you’ve lost money to someone. Hopefully some of the names are for retirement and savings. This is called zero-based budgeting where income minus outgoing equals exactly zero every single month. In other words, this month’s income is matched up exactly with bills, savings, and debt payments and every one of them have been given a name. There are plenty of programs online or phone apps that track this for you, but you should start right now, today, by writing it on the nearest piece of paper. Honesty and holding yourself to account is important.

The money saving guru Clark Howard says, “the first and most important part of your financial plan will always be expenses.” Most people have no idea how to balance a checkbook or how much they spend on things each month.

If you haven’t already, take it a step further and create a written financial plan. Now that you have given pencil to paper and know incoming dollars and outgoing dollars each month it’s time to use this tool for your benefit. In its simplest form, the plan will show you where you are, where you are going and what it will take to get there. If you are going to outsource this activity, I recommend using a Certified Financial Planner (full disclosure: I am one). If you are a do-it-yourselfer, make sure you are using software that runs Monte Carlo simulations to stress-test market volatility. Update your plan each year.

If you haven’t already, take it a step further and create a written financial plan. Now that you have given pencil to paper and know incoming dollars and outgoing dollars each month it’s time to use this tool for your benefit. In its simplest form, the plan will show you where you are, where you are going and what it will take to get there. If you are going to outsource this activity, I recommend using a Certified Financial Planner (full disclosure: I am one). If you are a do-it-yourselfer, make sure you are using software that runs Monte Carlo simulations to stress-test market volatility. Update your plan each year.

How are we supposed to save and invest when we barely get to the next payday? I just told you, write it down.

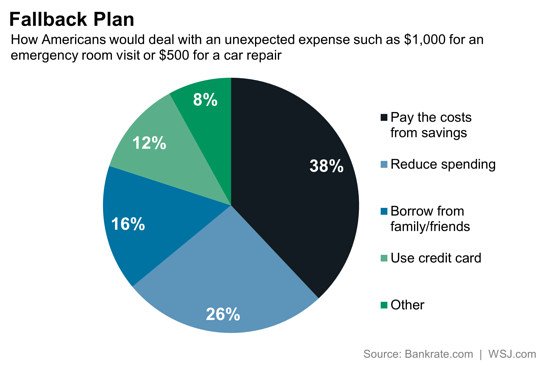

The Wall Street Journal reports that 70% of Americans are living paycheck to paycheck and wouldn’t have money in their savings accounts to pay for an unexpected car repair or medical emergency. My first thought is, what are the other thirty percent doing?

Break the cycle, live on less than you make and save for rainy days. Pull yourself up today into that 30% and email us or call when you need some extra guidance.

Blake Parrish

Senior VP, Portfolio Manager

Phone: (503) 619-7237

E-mail: blake@bpfinancialassoc.com

Certified Financial Planner Boardof Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.”