How much money will you need for retirement? Who hasn’t wrestled with that retirement question? But many people don’t know the answer. Forty-five percent of people just guess how large their nest egg must be, according to the 2013 Employee Benefit Research Institute survey.

Yet relying solely on guesswork can be a path to disappointment for golf professionals.

Building a big retirement nest egg can be even more of a challenge if you use faulty strategy. And many young investors do just that. Seventy-six percent of Americans ages 15-24 – admit they know little or nothing about how to invest, according to a new survey by brokerage TD Ameritrade. Nearly half – 47% – believe a savings account is the best way to prepare for retirement. I empathize with them, witnessing first-hand the effects on my family after the Tech bubble fifteen years ago followed by a stock market financial meltdown a few years later coupled with many families losing equity in the homes they live in.

Yet historically cash like that in a bank account dramatically underperforms stocks and many other asset classes. Investors need to own things, period. Even once interest rates rise back to normal levels around 4%, savings accounts will earn far less than other asset classes you can own as an investor.

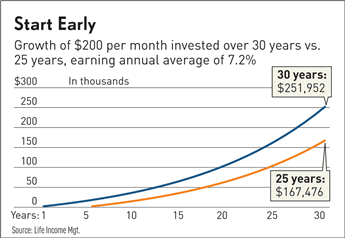

This generation is risk-averse. In other words, they don’t appreciate that stocks earn far more (over time) and are the best way to save for retirement. A simple chart shows this:

Okay, you don’t have $200 bucks a month laying around because we work in the golf business, right? You may have said, “Once I’ve made it to Director of Golf, I’ll catch up on my saving for retirement”. Get on it, then! Get educated in the PGA or develop your credentials through The Golfing Machine or TPI. Call Carol Pence, PGA Employment Consultant, right now -today to schedule a time to discuss your most valuable asset – YOU. All are terrific resources available to anyone willing to simply “make it happen”. What about on the spending side? That monthly cable bill, extra drink & desert decisions while eating out, or cell phone bill you seem to be able to afford. Do you really need these right now in your life?

Own anything, such as equity in a home, so that market volatility or job loss doesn’t catch you by surprise where the bank can come take your home via foreclosure. Own a duplex and rent out one side while living in the other. Own stocks, bonds, or other investments and try your best to make sure they are profitable companies and better yet can afford to pay investors a dividend to showcase the company’s financial strength.

My advice is to save first, then invest. And why not be more frugal. I’d rather have $100k in an account than drive a new car on lease, rent an expensive apartment, borrow on credit cards, etc. The benefits of living on less than what you bring in, and investing early is huge. Compounding magnifies stocks’ outperformance each year.

From 1926 through 2014, stocks averaged a 10.12% annual return and have never had a rolling 15-year period of negative nominal returns. Don’t get caught up in all of the historical numbers because people are not typically invested 100% in an index fund tracking the S&P500, but rather start with target date types of funds. Better yet, hire an advisor to be selective with the investments inside of your portfolio.

Blake Parrish

Senior VP, Portfolio Manager

Phone: (503) 619-7237

E-mail: blake@bpfinancialassoc.com